Legal Bites #03 | IFICI – Incentive for Scientific Investigation and Innovation

The new Incentive for Scientific Investigation and Innovation (IFICI) is Portugal’s latest national mechanism to attract and retain highly skilled talent, while supporting a knowledge-based economy, technological innovation, and digital transformation.

Within this framework, Startup Portugal is responsible for recognizing companies as startups, as well as verifying the requirements related to the activities carried out by taxpayers applying for IFICI.

What is it?

IFICI is a tax incentive aimed at individuals who move to Portugal and carry out eligible scientific research or innovation activities. In the case of startups, the benefit depends on the prior recognition of the company as a startup under Law No. 21/2023, of May 25.

Eligibility

To benefit from IFICI, the taxpayer must cumulatively meet the following criteria:

- Hold an employment contract or be a member of the management body (manager or director) of a legally recognized startup;

- Be directly involved in scientific research or innovation activities;

- Have become a resident of Portugal in accordance with Article 16(1)(a) and (b) of the Personal Income Tax Code (CIRS);

- Not have been a resident of Portugal in the preceding five years;

- Not currently benefit, nor have previously benefited, from the Non-Habitual Resident (RNH) regime;

- Not currently benefit, nor have previously benefited, from the Programa Regressar.

The benefit depends on the prior recognition of the company where the activity is carried out as a startup, in accordance with Law No. 21/2023, of May 25.

All information about the startup/scale up recognition process can be found here.

What is the tax benefit?

Taxpayers who meet all legally established criteria may benefit from:

- A 20% flat personal income tax (IRS) on income earned from activities carried out within the startup, for a period of 10 years, starting from the year in which they became a resident of Portugal;

- An exemption on income earned abroad, provided it does not originate from a jurisdiction with a clearly more favorable tax regime, for income in categories A, B, E, F, and G, with such income being mandatorily aggregated for the purpose of determining the applicable tax rate on the taxpayer’s remaining income.

How to submit the application – step by step

To register for the IFICI, the taxpayer must:

- Confirm that the company in which they are employed, or in which they serve as a member of a management body while performing scientific research or innovation activities, is recognized as a startup, in accordance with Law No. 21/2023, of May 25;

- Have a copy of the individual employment contract, or an up-to-date permanent commercial certificate, as applicable to their specific case;

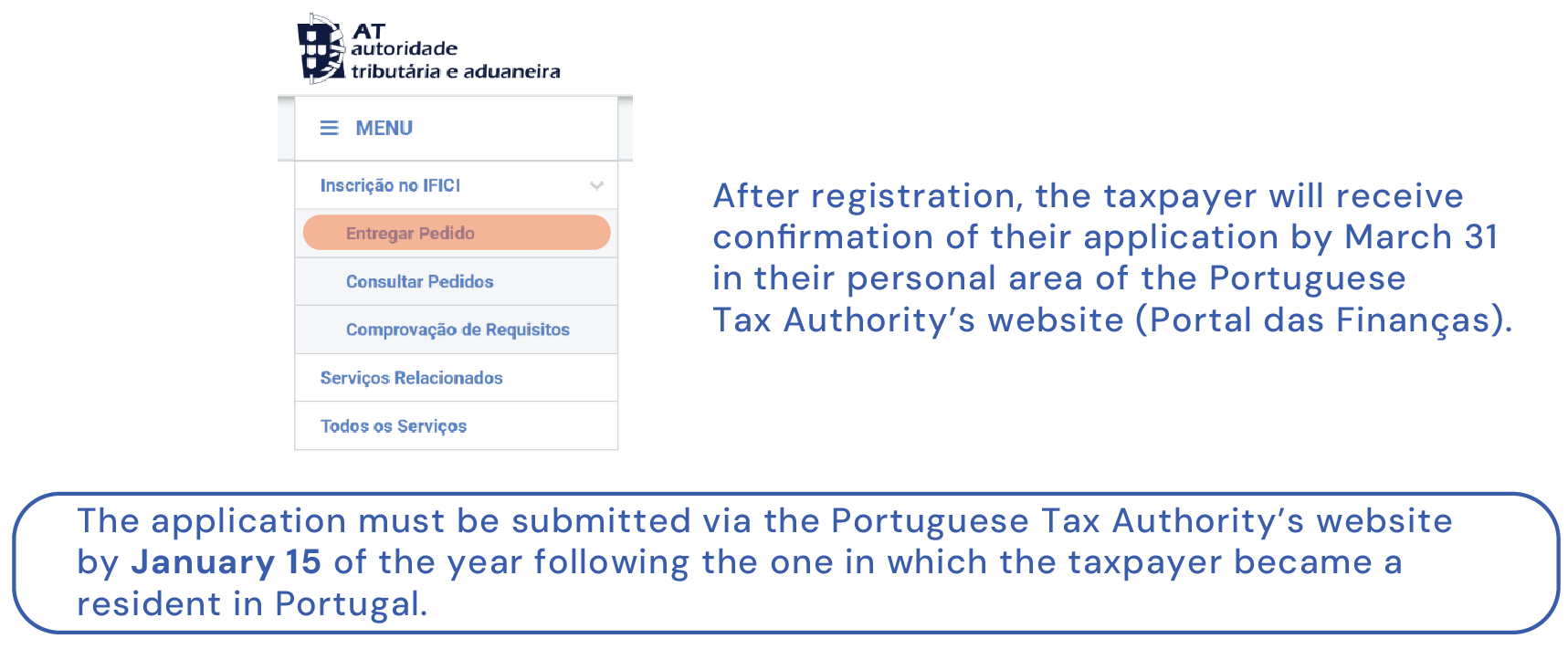

- Submit the application through the personal area of the Portuguese Tax Authority’s website (Portal das Finanças), under “Inscrição no IFICI” → “Entregar Pedido”.

Frequently Asked Questions

I am an employee of a startup and benefit from the IFICI. In addition to my employment income from that company, I hold shares in a company domiciled in a jurisdiction with a clearly more favorable tax regime, which distributes dividends annually. How will I be taxed?

Employment income is taxed at the special rate of 20%. Dividends distributed by a company domiciled in a country subject to a clearly more favorable tax regime are taxed at a rate of 35%.

What is the duration of the IFICI?

The IFICI applies for 10 consecutive years. In the event of an interruption, it may be resumed for the remaining years, provided that the beneficiary again becomes a tax resident in Portugal and once more earns income covered by the IFICI regime.

Example: A taxpayer obtained IFICI status in 2024 and benefited from it until 2028 (five years), then resided in another country in 2029. In 2030, they became a tax resident in Portugal again, engaging in one of the activities covered by the IFICI. In this case, the taxpayer may resume the IFICI for the remaining four years, that is, from 2030 to 2033.

What should I do if I no longer meet the IFICI requirements?

The beneficiary must notify the authorities by January 15 of the year following the change. The right to the tax benefit ceases on the date when the legal requirements are no longer met.

What should I do if any requirement or element of my registration changes, but I continue to benefit from the IFICI, for example, in another company?

Whenever there is a change in the information provided in the registration, namely regarding the company for which the taxpayer works, the taxpayer must report the change through the Tax Portal (Portal das Finanças) by January 15 of the year following the alteration.

Example:

- On January 15, 2025, the taxpayer began a teaching activity at a higher education institution, which ended on June 15, 2026;

- On September 15, 2026, the taxpayer began a new activity at a startup;

- Since the new activity began within six months after the end of the previous one, the taxpayer retains the right to the IFICI;

- The taxpayer must report this change through the Tax Portal by January 15, 2027, by submitting a new registration request.

Relevant Legislation

- Law No. 21/2023, of May 25;

- Article 58-A of the Tax Benefits Statute (EBF);

- Articles 16 and 81 of the Personal Income Tax Code (Código do IRS);

- Ordinance No. 352/2024/1, of December 23, in its current wording;

- Ordinance No. 150/2004, of February 13, in its current wording.

Can you handle more than one Legal Bite?

Explore our LEGAL BITES series, where we break down legal and tax topics that impact startups in Portugal. Ready for another bite? Check our other Legal Bites here.

Note: This content is for informational purposes only. For tailored advice, please consult a qualified professional.

Other blog posts